Convertibill are an Irish lending platform that are expanding in to the UK. They provide working capital finance against confirmed orders from credit worthy buyers and also against outstanding invoices.

As business finance brokers Funding Solutions UK Ltd have had a few dealing with Convertibill and it would be fair to say that they have not gone well. It would also be fair to say that we won’t be having any more dealings with them. I would question their honesty and integrity for a few reasons. Here is a brief description of some of our interactions:

We introduced a client who provided specialist type of marine funding. Convertibill signed an NDA as the client was worried that their product would be copied. Convertibill requested more and more information and the client was suspicious that they were merely trying to obtain information from them so they could copy their approach or learn more about how to fund this type of transaction. When the client raised this the enquiry was closed down and they refused to acknowledge the signed NDA. Patrick Reynolds CEO advised, “There is no NDA from June” and despite sending him a copy of the signed NDA he refused to acknowledge it. Our client is now taking legal advice.

We introduced another client who was looking to bridge an investment transaction that included funding from the Future Fund. Convertibill advised that they could help but that they required a £15,000 commitment fee to start the process. The client paid the £15,000 and then asked if they could change the transaction. This request was the next day. Convertibill advised that they could no longer assist and that they had spent the £15,000 on legal fees and on securing the required funding. In my opinion this is a nonsense and is pure profiteering. Again, our client is taking legal advice.

As a finance broker I earn money from setting up finance facilities for my clients. I had referred a client to Mark Runiewicz of Convertibill and specifically request that he provided a stand alone trade/purchase finance facility for the client as they were happy with their invoice finance provider. Mark entered in to talks with the client and then introduced them to 3 invoice finance providers. These 3 lenders were Skipton Business Finance, Optimum Finance and Gener8. We were never advised of this by Mark but they client alerted us to this. Strangely, Mark then claimed that Convertibill had now started to fund against debtors and that they would fund the full transaction. It is my opinion that Mark was trying to broker this invoice finance requirement for himself. With one lender I checked with the lead was logged in the name of Mark’s business SC Advisors Limited who would have received the commission had the transaction completed. Putting our situation to one side it seems strange that Mark is employed by Convertibill but is introducing an invoice finance requirement to other lenders. Even more strange when you consider that is what we do as a business!! Market Finance were the incumbent invoice finance provider and they refused to work with Mark Runiewicz and Convertibill. At the time this seemed harsh to me but having done some investigation it appears they may have been concerned with Mark’s previous involvement with other P2P lenders via his business UK Exim Finance Limited and UK Exim Limited. The information at Companies House would suggest that these relationships did not end well. Type these business names in to Google and look at the filing history at Companies House. It appears that lenders lost money and a significant amount due the activities of these businesses.

Something really doesn’t feel right about Convertibill. My advice would be to proceed with extreme caution. Arguably, there are other options out there so maybe explore those.

If you are reading this as a fellow business finance broker I would also proceed with extreme caution. There are questions about how client introductions are handled but I also have reason to believe that they work hard to find ways not to pay broker commissions and may indeed pride themselves on their ability not to pay brokers. At a senior level within the business there seems to be a dislike for brokers and a willingness to find ways not to pay brokers the agreed fees.

Updated 5 October 2020.

I was approached by Convertibill and asked to take the post down. The initial conversation included a threat of legal action for libel if I did not take it down within 24 hours. With a view to learning more about their side of the story and as a gesture of goodwill I took the post down. However, whilst explanations were offered they did not change my opinion of what occurred. What I have posted is based on my honest opinion.

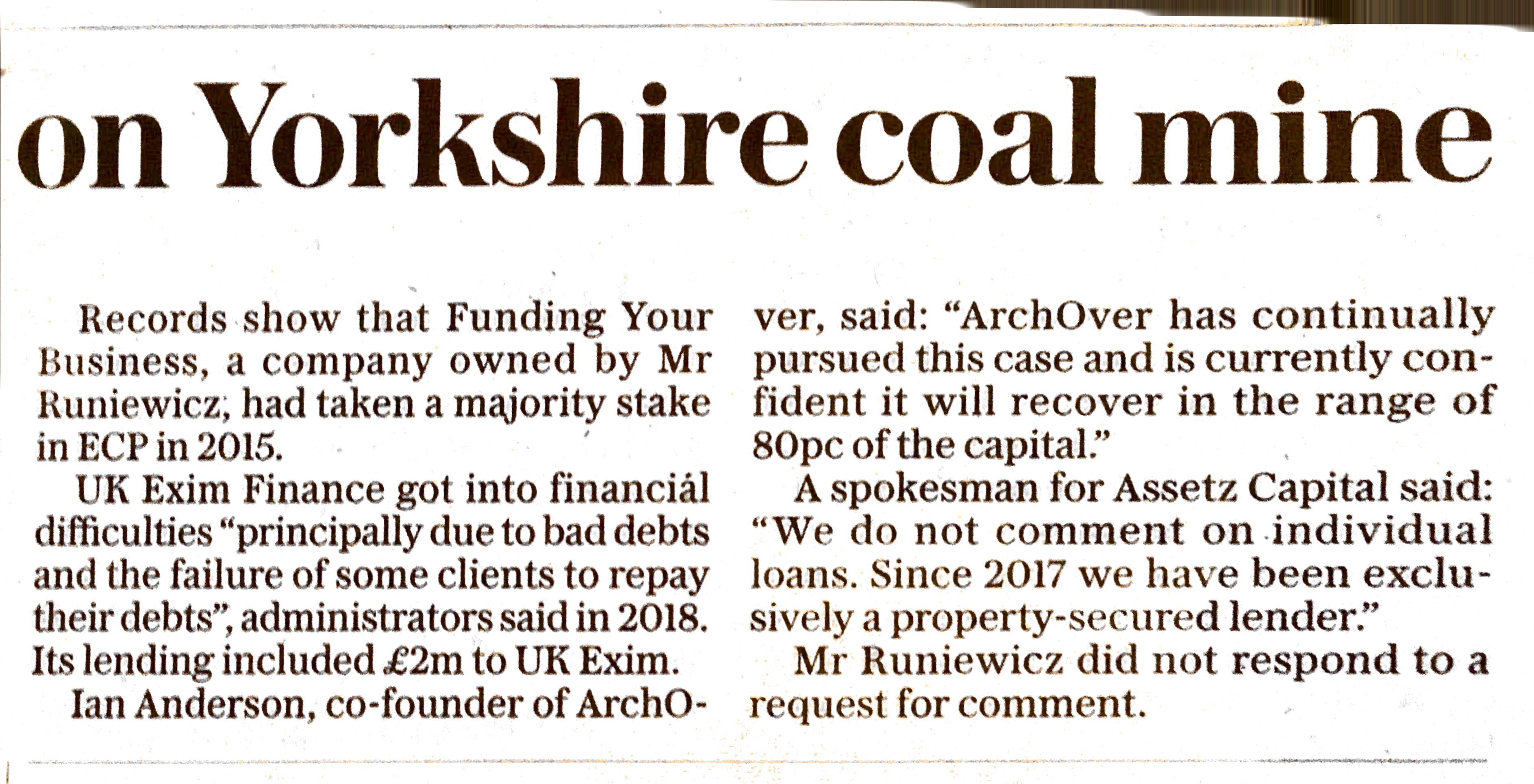

In addition, there has been an article published in the Telegraph on 2nd October 2020 about the businesses that Mark Runiewicz has run and the potential losses they have caused in the P2P lending sector. The articles are in the images below: